On March 24, 2000, the New England Patriots broke ground on their new stadium home in Foxborough, Massachusetts. The internet company CMGI won naming rights, agreeing to pay $114 million over 15 years for the privilege. The 2002 season opened on September 9 in the Patriots’ new home, tickets bearing the name, CMGI Stadium.

On March 24, 2000, the New England Patriots broke ground on their new stadium home in Foxborough, Massachusetts. The internet company CMGI won naming rights, agreeing to pay $114 million over 15 years for the privilege. The 2002 season opened on September 9 in the Patriots’ new home, tickets bearing the name, CMGI Stadium.

Except by that time, the “Dot-Com” bubble had burst. CMGI had ceased to exist. The stadium itself would open, bearing the name of a razor and shaving cream manufacturer.

Economic forces had combined with irrationality to bid up prices to the point of collapse, but this was neither the first nor the first time. We saw it in the housing bubble of the 2000s, and the “Bull Market” of the Roaring 20s.

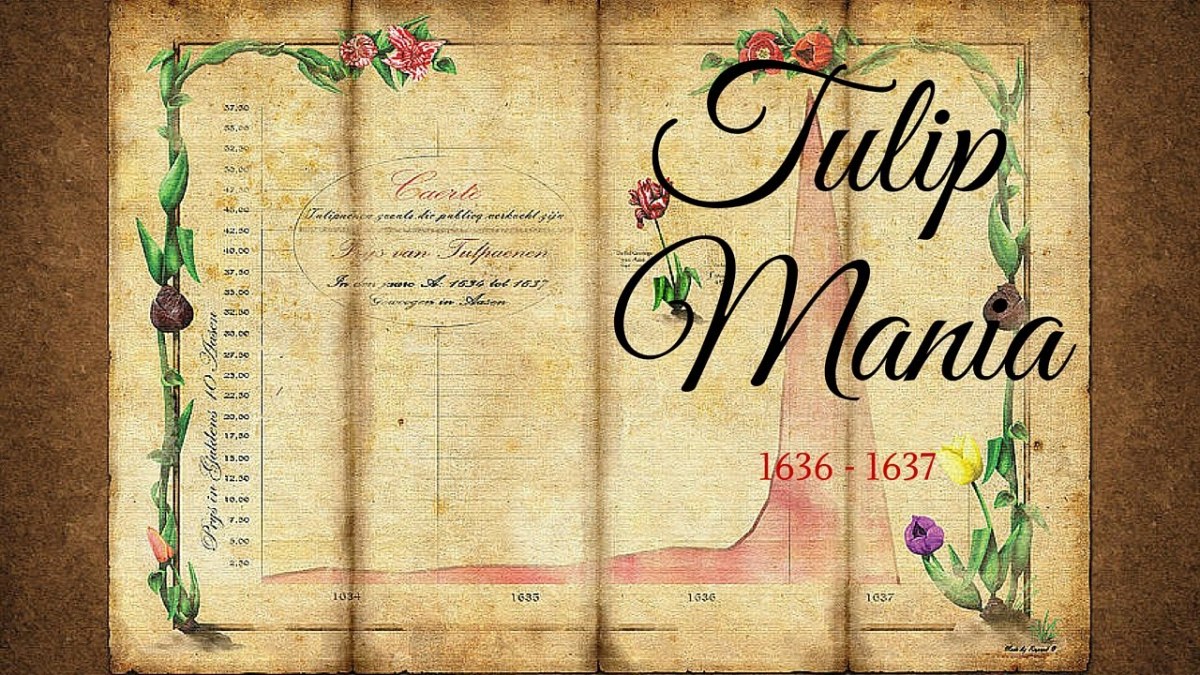

The oddest of these speculative bubbles may be the “Tulpenwoede” (tulip madness) gripping Holland in the 17th century.

The first tulip bulbs came from the Ottoman Empire to Vienna in 1554, introduced to Europe by Ogier de Busbecq, ambassador of the Holy Roman Emperor Ferdinand I to the Sultan of Turkey. The tulip was different from anything in Europe, the intense, saturated colors soon turning the flower into a status symbol.

By the 17th century Holland had embarked on a Golden Age. The East Indies trade  produced single voyage profits of 400% and more, as merchants built grand estates surrounded by flower gardens. The hyacinth enjoyed early popularity, but the plant at the center of it all was the spectacular, magnificent, tulip.

produced single voyage profits of 400% and more, as merchants built grand estates surrounded by flower gardens. The hyacinth enjoyed early popularity, but the plant at the center of it all was the spectacular, magnificent, tulip.

For much of this period, tulip bulbs were primarily of interest to the wealthy. The craze began to catch on with the middle and poorer classes by the mid-1630s. Soon, increased demand began to drive prices to irrational levels.

The market soared in late 1636, as prices bid up for bulbs planted to bloom the following spring. People mortgaged their homes and businesses, hoping to buy bulbs for resale at higher prices. At one point, “one single root of the rare species called the Viceroy”, sold for “two lasts of wheat, four lasts of rye, four fat oxen, eight fat swine, twelve fat sheep, two hogsheads of wine, four tuns (barrels) of beer, two tuns of butter, One thousands lbs. of cheese, one complete bed, a suit of clothes, and a silver drinking-cup”. In early 1637, single “Viceroy” bulbs bid between 3,000 and 4,200 guilders, at a time when skilled craftsman earned about 300 guilders a year. At one point, 5 hectares (12 acres) of land were offered for a single Semper Augustus bulb.

“Couleren” bulbs were most commonly traded, single hued flowers of yellow, red or white, followed by the multi-colored “Rosen” and “Violettin”. Rarest and most sought after were the vivid streaks of yellow or white on the red, brown or purple backgrounds of the “Bizarden” (Bizarres). Ironically, these were the most sickly specimens, victims of a “Tulip breaking virus” which “broke” petals into two or more hues.

the vivid streaks of yellow or white on the red, brown or purple backgrounds of the “Bizarden” (Bizarres). Ironically, these were the most sickly specimens, victims of a “Tulip breaking virus” which “broke” petals into two or more hues.

Confidence evaporated in 1637 and the market collapsed. The last recorded market data were reported on February 5, as 98 sales were recorded at wildly varying prices. Those who had taken possession of bulbs found their worth to be a fraction of the prices paid. Others were locked into futures contracts, obliged to pay ruinous sums for comparatively worthless flower bulbs.

Afterward

Today, the Federal National Mortgage Association (FNMA), and Federal Home Loan Mortgage Corporation (FHLMC), are Congressionally authorized hybrids or “GSEs” (government-sponsored enterprises), charged with “providing liquidity and stability to the U.S. housing and mortgage markets”. Better known as “Fannie Mae” and “Freddie Mac”, both entities are privately owned by shareholders and backed by taxpayers.

The US Department of Housing and Urban Development (HUD) was charged with regulating Fannie and Freddie in 1992. Before that, these organizations were required to buy only “prime” mortgages, notes which institutional investors would buy on the open market. Such standards made it too difficult for lower income, higher risk buyers to become homeowners, or so it was believed. Regulators imposed “affordable housing”  guidelines that year, imposing a 30% quota and raising it to 50% by the end of the Clinton era. By 2007 under President Bush, 55% of all mortgages purchased by the mortgage giants were “sub-prime”.

guidelines that year, imposing a 30% quota and raising it to 50% by the end of the Clinton era. By 2007 under President Bush, 55% of all mortgages purchased by the mortgage giants were “sub-prime”.

Banks and brokers were happy to sing along, issuing “NINJA” loans (No Income No Job no Assets) to anyone who asked. “Low-doc” and “no-doc” mortgages called “liar loans” sprouted up everywhere, but gone were the days when your home town bank held your mortgage. No mortgage originator would ever be left holding the bag, should these loans turn bad. They sold them to Fannie and Freddie.

Fannie, Freddie and others “bundled” high risk mortgages into increasingly exotic financial instruments called “mortgage backed securities”, selling them off to investors and backing transactions with “credit default swaps” (CDS), a two-party agreement impossible to distinguish between an insurance contract and a bet.

The danger signs were there for those who would see, but Barney Frank said it best in 2003: “I want to roll the dice a little bit more in this situation toward subsidized housing.”

2003: “I want to roll the dice a little bit more in this situation toward subsidized housing.”

Property values doubled and doubled again. You were always going to make money in real estate. Family members sold to one another over and over at ever increasing prices, with none ever moving out of the house. Aggregate CDS values reached $62 Trillion in 2008, equivalent to a stack of dollar bills, reaching from Earth to the moon. 18 times.

Then, the bubble burst. Imagine waking one morning to find your entire pension or mutual fund account, was invested in that stuff.

That was the year when gas first hit $4/gallon. Those living closest to the financial cliff began to fall off, and foreclosures went through the roof. Highest risk mortgage holders were the first to default, people with $20,000 incomes and multiple investment properties. We all remember 2009. I myself lost a job of 15 years when my employer went under, briefly making my family part of the “zero percent”. Some will tell you that we haven’t emerged from the “Great Recession”, to this day.

That was the year when gas first hit $4/gallon. Those living closest to the financial cliff began to fall off, and foreclosures went through the roof. Highest risk mortgage holders were the first to default, people with $20,000 incomes and multiple investment properties. We all remember 2009. I myself lost a job of 15 years when my employer went under, briefly making my family part of the “zero percent”. Some will tell you that we haven’t emerged from the “Great Recession”, to this day.

The old subprime “MyCommunityMortgage” program is dead and buried, but not the geniuses who gave it life. Sub-prime has become a dirty word, so, until recently, regulators pushed “alt” mortgage guidelines. Once, your “income” had to be your own, whether or not you could document it. Now, you could claim other people’s income: your aunt, parents, even a roommate. They won’t be on the note, they have no responsibility to repay. They don’t even have to live there. As long as you can augment your income enough to qualify. What could go wrong with that?

Speaking of the Patriots, I hear there’s a game today. I’ll have to check it out. At this point, I’d rather think about football.

Go Patriots.

You must be logged in to post a comment.